Archive

AI – rescuing the spectrum crunch (Part 1)

Chamath Palihapitiya, the straight talking boss of Social Capital recently sat down with Vanity Fair for an interview where he illustrated what his firm looked for when investing. “We try to find businesses that are technologically ambitious, that are difficult, that will require tremendous intellectual horsepower, but can basically solve these huge human needs in ways that advance humanity forward”.

Around the same time, and totally unrelated to Chamath and Vanity Fair, DARPA, the much vaunted US agency credited among other things for setting up the precursor to the Internet as we know it threw up a gauntlet at the International Wireless Communications Expo in Las Vegas. What was it: it was a grand challenge – ‘The Spectrum Collaboration Challenge‘. As the webpage summarized it – “is a competition to develop radios with advanced machine-learning capabilities that can collectively develop strategies that optimize use of the wireless spectrum in ways not possible with today’s intrinsically inefficient static allocation approaches”.

What would this be ‘Grand’? Simply because DARPA had accurately pointed out one of the greatest challenges facing mobile telephony – the lack of available “good” spectrum. In doing so, it also indirectly recognized the indispensable role that communications plays in today’s society. And the fact that continuing down the same path as before may simply not be tenable 10 – 20, 30 years from now when demands for spectrum and capacity simply outstrip what we have right now.

Such Grand Challenges are not to be treated lightly – they set the course for ambitious endeavors, tackling hard problems with potentially global ramifications. If you wonder how fast autonomous cars have evolved, it is in no small measures to programs such as these which fund and accelerate development in these areas.

Now you may ask why? Why is this relevant to me and why is this such a big deal? The answer emerges from a few basic principles, some of which are governed by the immutable laws of physics.

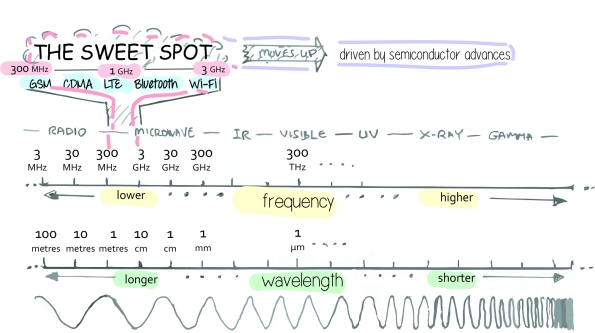

- Limited “good” Spectrum – the basis on which all mobile communications exists is a finite quantity. While the “spectrum” itself is infinite – the “good spectrum” (i.e. between 600 MHz – 3.5 GHz) or that which all mobile telephones use is limited, and well – presently occupied. You can transmit above that (5 GHz and above and yes, folks are considering and doing just that for 5G), but then you need a lot of base stations close to each other (which increases cost and complexity), and if you transmit a lot below that (i.e. 300 MHz and below) – the antenna’s typically are quite big and unwieldy (remember the CB radio antennas?)

Courtesy: wi360.blogspot.com

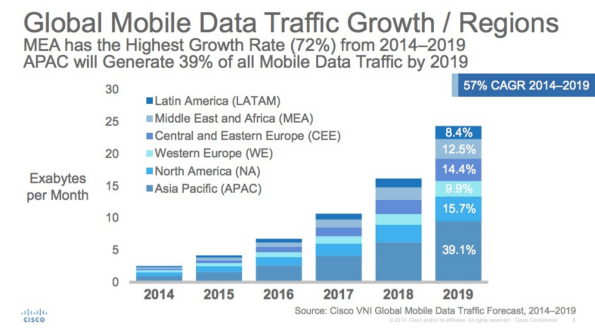

- Increasing demand – if there is one thing all folks whether regulators, operators or internet players agree upon it is this; that we humans seem to have an insatiable demand for data. Give us better and cheaper devices, cool services such as Netflix at a competitive price point and we will swallow it all up! If you think human’s were bad there is also a projected growth of up to 50 Bn connected devices in the next 10 years – all of them communicating with each other, humans and control points. These devices may not require a lot of bandwidth, but they sure can chew up a lot of capacity.

CISCO VNI

- and as a consequence – increasing price to license due to scarcity. While the 700 MHz spectrum auction in 2008 enriched the US Government coffers by USD 19.0 Bn (YES – BILLION), the AWS-3 spectrum (in the less desirable 1.7/2.1 GHz band) auction netted them a mind-boggling USD 45.0 Bn.

One key element which keeps driving up the cost of spectrum is that the business model of all operators is based around a setup which has remained pretty much the same since the dawn of the mobile era. It followed a fairly, well linear approach

- Secure a spectrum license for a particular period of time (sometimes linked to a particular technology) along with a license to provide specific services

- Build a network to work in this spectrum band

- Offer voice, data and other services (either self built) or via 3rd parties to customers

While this system worked in the earlier days of voice telephony it has now started fraying around the edges.

- Regulators are interested that consumers have access to services at a reasonable price and that a competitive market environment ensures the same. However with a looming spectrum scarcity, prices for spectrum are surging – prices which are indirectly or directly passed on to the customer

- If regulators hand spectrum out evenly, while it may level the playing field for the operator it does nothing to address a customer need – that the capacity offered by any one operator may not be sufficient… leaving everyone wanting for more, rather than a few being satisfied

- Finally, the spectrum in many places around the world remains inefficiently used. There are many regions where rich firms hoard spectrum as a defensive strategy to depress competition. In other environments there are cases when an operator who has spectrum has a lot of unused capacity, while another operator operates beyond peak – with poor customer experience. No wonder, previous generations of networks were designed to sustain near peak loads – increasing the CAPEX/ OPEX required to build up and run these networks.

In the next part of this article we will dive deeper into these issues, trying to understand how an AI enabled dynamic spectrum environment may work and in the last note point out what it could mean to the operator community and internet players at large…..

Pebble – mounting troubles in the wearable space

4 days ago, Pebble announced a massive round of layoffs with ~25% of the firm being given the pink slip. In a statement, CEO Eric Migicovsky pointed out to an increasingly difficult funding environment which limited its options to grow and expand. This was a very different situation from just over a year ago when Pebble broke not one, but two kickstarter records – raising the fastest million in 49 minutes and the highest amount in fund-raising, raising $13.3 m (a total of $20,336,930 from 78,463 people over two iterations).

As a curious onlooker into the wearable space, and keenly aware that apart from my super early adopter friends, few if any (especially outside the US) have heard about Pebble I have increasing doubts on the viability of the firm in its present state, however innovative it may have been. A few reasons point to this which I will try and illustrate.

- Flop of the Apple Watch: For all its hype the behemoth in this market, the one that everyone hope would raise the profile of wearables – Apple, has fallen way short of expectations. While Apple proudly announced the sale of 48m iPhones in 1 quarter, it declined to state the number of watch sales….. maybe nothing to crow home about. Add to the fact that Apple has itself dropped the price does not bode well for the product in its present form. While Apple can afford such failures while sitting on billions of cash, Pebble with its limited financial power and debt burden – cannot.

- Entry of competitively entrants with an established eco-system: at the recently concluded MWC in Barcelona, Chinese manufacturers such as Huawei launched several native Android wearables. These actually look quite good, and best of all – already have over 3000 apps on the Google Play store. Maybe items such as e-ink with a longer battery life like Pebble are good to have, but by now users are getting accustomed to charge their devices regularly – adding a watch to the mix isn’t a huge behavior change. While Pebble did announce an entry into India in partnership with Amazon, I fail to see how this can change their fortunes. In India – those who have money can and will buy an Apple watch; those that don’t… well they will look at their options, and for the Indian market, Pebble isn’t the cheapest smart watch around. Pebble would have to go below $40 for it base model to even hope to make a difference.

- Lack of an ecosystem: I think this is one of the biggest challenges that Pebble faces. Microsoft and Blackberry faced (and continues to face) the same challenge with its Windows phones. Without a healthy and growing ecosystem it will always be an uphill battle to attract customers. Apple’s success is testament to this – it was clear that while Apple perhaps would never match Samsung and the others in pure feature set, what set it apart was good design, intuitive UI/ UX and an expansive ecosystem. Remove one of these elements from the mix and you quickly fell to the way-side. And if you closely look at Pebble’s ecosystem it is wanting both in terms of quality (ratings) and quantity.

- Limited user benefit: this one brings the point home. Similar to the Apple watch, most people haven’t yet found compelling use cases in this space; they are “good to have”… not “must haves”. Those that are early adopters already have it, those who are followers can now consider a cheaper Apple watch, or from a plethora of Google gear at different price points. What you end up with is a niche who either hate Apple and Google or simply want to be different. Is this market big enough to support Pebble – and do so now? Or is this market still in a nascent phase and needs time – which Pebble may not have?

I do feel sorry for Pebble, I really do. Hardware is hard enough, building hardware and a viable ecosystem only compounds the problem. While it is admirable (and we do need brave firms such as these) to innovate in spite of these challenges, without a long term plan (and backing) along with a solid team I feel that Pebble is faced with an insurmountable and impossible task. The only solace I do have is for their employees (both current and past); those adventurous souls who took the path less traveled. The wearable industry will continue to grow and the skills and learning that they have gained here will make them highly sought after in an increasingly competitive environment for talent.

The dynamic pricing game – where all is not 99c

Phil Libin the effervescent CEO at Evernote made headlines two days ago when he admitted that Evernote’s pricing strategy had been a bit arbitrary and a new pricing scheme for their premium offering would be launched come 2015. Although little was said about what the approach would be – I do hope it points to adopting a flexible pricing approach, and serve as a forerunner for pricing strategies to legions of firms down the road.

To put some context, many software providers (especially app companies) have adopted a one price fits all approach; i.e. if the price for the app is $5 per month in USA, the price is $5 per month in India. The argument has typically been one of these

- Companies such as Apple do not practice price differentiation around the world, and yet they sell – so we should also be able to do the same

- Adopting a one price fits all approach streamlines our go-to-markets and avoids gaming by users

- It is unfair to users who would end up paying a premium for a product which can be sourced for a cheaper price elsewhere

From a first hand experience I believe that such attitudes have proven to be the one of the biggest stumbling blocks for firms to achieve global success. A good way to explain why is to pry apart these assertions.

- The Brand proposition argument – Although every firm would love (and some certainly do in a misguided manner) to believe that their firm has a premium niche such as Apple – harsh reality points in a different direction. There are only two brands who top $100 bn – and Apple is one of them; and no – unless you are Google, you are not the other! Even though your brand may be well known in your home of Silicon Valley, its awareness most likely diminishes with the same exponential loss as a mobile signal – its value in Moldova for example – may be close to zero. This simple truth is that there are only a handful of globally renowned brands (e.g. Apple, Samsung, BMW, Mercedes, Louis Vuitton etc) which can carry a large and constant premium around the world.

- The “avoid gaming” argument – this does have some merit, but needs to be considered in the grand scheme of things. Yes – this is indeed possible, but is typically limited to a small cross section of users who have foreign credit cards/ bank accounts etc. The vast majority are domestic users who are limited to their local accounts and app stores. The challenge here is to charge the same fee irrespective of the relative earning power in a country. While an Evernote could justify a $5 per month premium in USA (a place where the average mobile ARPU is close to $40), it is very hard to justify it in South East Asia (mobile ARPU close to $2) or even Eastern Europe (mobile ARPU close to $8). It then would simply limit the addressable market to a small fraction of its overall potential – and dangerously leave it open to other competitors to enter.

| ARPU | $12.66 | $2.46 | $11.37 | $9.20 | $48.15 | $23.88 | $8.77 |

| Region | MENA | APAC | Oceania | LatAm | USA | W.EU | E.EU |

- The unfairness argument – also doesn’t hold true. The “Big Mac Index” stands testament to the fact that price discrimination is an important element of market positioning.

Even if you argue that you cannot buy a burger in one country to sell in another, the same holds for online software – take the example of Microsoft with its Office 365 software product, same product – different country – different price.

- That brings me back to the final point – $5 per month may sound like a good deal if you are a hard core user, but if you compare it with Microsoft Office 365 – which also retails at $5 per month, it is awfully hard to justify why one would pay the same for what is essentially a very good note taking tool.

Against this background, I do welcome the frank admission that this strategy is in need of an update, and also happy to hear that the premium path isn’t via silly advertisements. Phil brought up a good challenge with his 100 year start-up and delighted to know that he still is happy to pivot like one. I do for sure hope that the other “one trick pony” start-ups learn from this and follow suit.

Friction-free: enabling happy customers

Last week, I had the good fortune to attend MBLT 2014, a conference all around the rapidly evolving mobile ecosystem. Among the many speakers at the conference, two which piqued my attention were those from Spotify & SoundCloud; both speakers were engaging, and interestingly enough – both talked about growth.

When we talk about growth here, it wasn’t all about entering new markets, or creating new products. It involved a lot of small elements; elements which when brought all together ensured that you gained a lot of users and who kept coming back. Although Spotify and SoundCloud operate in the music space, both (currently) focus on different aspect of this segment. As Andy @ SoundCloud succinctly put it; if Spotify was the Netflix of music, then SoundCloud was Youtube. However, each company seemed to have a common approach when it came to customer acquisition – to develop a friction-less sign up process.

At its core it simply meant reducing the number of clicks, mouse moves etc required to sign up a user and/ or a customer. Both agreed that if any sector was to be considered as “best practice” then it would be mobile gaming – and the king of the hill was… well, King.com. The makers of Candy Crush had got this bang on – all you had to do is download the game and you were good to go.

Their mantra was -> Number of clicks to sign up = 0. Number of users = millions!

Both SoundCloud & Spotify were always on the lookout to make the whole signup process, simpler, quicker and more efficient – fully aware of the fact that complicated processes turned away prospective users, and getting them back wasn’t a trivial matter. That point got me examining different websites to see just how much this mattered (a study done by Spotify as well). After some pottering around, I couldn’t but wholeheartedly agree with the rationale of such an approach.

If you now compare this mentality with IT solutions at traditional corporations you realize how far behind the curve they are in this respect. Many systems there are built more with the paranoia of security and little consideration for user engagement. These are what I call “push systems” – where employees have no choice BUT to use these services mandated by IT. The direct result is that either personnel shy away from using these services, or doing so becomes an irritating chore (especially since they use better designed services on a daily basis). Rather than a full scale rebellion, we are seeing services which simply assist existing ones services such as Brisk.io gaining traction because continuously updating SalesForce is tedious.

A takeaway would be for IT personnel to closely work with end users in deciding how they would like to engage with the services they use on a daily basis. Focusing on small but important elements such as “clicks to complete entries” etc will make employees more enthusiastic on using such services making these more an aid (which was the purpose) rather than a chore!

The user (UN)experience

I cannot claim to be a customer sales or usability expert, but a personal experience just this past week acutely brought to the forefront of how important and relevant a good customer and user experience is – both to keep a customer and protect the reputation of a firm. Sharing this not as a matter of criticism since I cannot blame any party (they were simply following rules) but hopefully to open the eyes of those that make these decisions which need to be followed.

I found myself in Germany, and needing an internet connection went to pick up a data SIM. I had a router (one of those which would take in a 3G signal and provide a WiFi output) and figured that all I needed was a SIM card with a few Gigabytes of data which could be recharged at will. I had done this all over the world – from Saudi Arabia to South Africa so figured that this would be a 5 minute, grab and buy exercise. It turned out everything but that.

For starters, the operator actually didn’t seem to have such an offering, a bit odd since I would expect that this would be the bread and butter business of a Telecom provider. Or perhaps he did but the sales personnel didn’t seem to quite find the right product. If I may note – he had to peruse through a thick manual, I couldn’t blame him if he himself didn’t know the product existed or not. But all was not lost, as he pointed out a cheaper alternative provided by their no-frills subsidiary. It came with a USB stick as well which I didn’t quite need but he assured me that once activated I could transfer the SIM card to my router.

Then the fun started. Once I came back to my desk (thankfully close to the shop) I figured out that in order to use the device I needed to activate the SIM – and the main way to activate the SIM was to go online and register. Made me wonder a bit – if you wanted a data-stick, then perhaps you did NOT have a means to go online in the FIRST place! This was never the case anywhere else in the world, wondered why it was a requirement in Germany.

Did that – but still nothing. I duly returned back to the shop and pointed out my dilemma. To their credit they quickly set me up with a trainee technician who knew English. But then there was another ‘issue’. According to strict protocol since this was a ‘no frills’ sub-brand they didn’t actually provide any support. In addition – if I did ask for support in installation then I would have to pay ‘extra’ for this service. Again a bit strange, since if the device wasn’t proving to be as simple to operate as the manual said – and no support was provided then what use is the device in the first place! But again, with a bit of coaxing, the tech support got permission to assist me for ‘free’. Now we figured out that we needed to install a new driver and you needed to be …. (you guessed it) ONLINE to download it. Oh well, it now seemed that to use the device you needed to be online in the first place!!!

We worked on that from his machine – and still no luck. We had now activated the SIM and installed the update but apart from a flickering green light there was no sign of life. The Tech support called his supervisor who tried using another dongle – same result. We then researched on Google to figure out the problem – from perusing forums its seemed that the drivers did not work with 64 bit systems – even stranger since most modern OS used it. So perhaps, this was made for older laptops…. in that case why keep it? We got on the phone with the subsidiary in an attempt to explain the problem so that I could return it – but from what I gathered they were very reluctant to do so, and the store seemed to have a no return policy for such a device.

I came back the next day, one night of trying had led to no success, the technician although wanting to take back the device was limited from what he could do. I have been asked to come back to speak to a ‘Business Manager’ on the following day.

This brings me back full circle to why I posted this – maybe it is a bit of venting some frustration, but it also the seemingly lack of thought for the user experience in the design of the product. From the customer support personnel, it is the sad acknowledgement that although they can help, their hands are tied and we have to escalate several levels to hope for resolution. Shouldn’t it be the case that if for a brand new product that refuses to function as designed, even though thoroughly tested by their own technicians there should be a no questions asked return policy, instead of forcing the customer to repeatedly revisit their store.

The company would be poorer in that respect – losing a customer who determines that some of the products are badly designed, the support staff are unable to provide the support he needs. They may be $20 richer in selling me a non-working device, but several orders of magnitude poorer in reputation. Long term value – is thus eroded

The disappearing SIM

If there is one piece of telecom real-estate that the operator still has a strangle hold on then it is the end customer – and the little SIM card holds all the data of the customer. Interestingly enough, that as the smart-phones continue to grow in size (some of them would definitely not fit in my pocket anymore) the SIM card appears to be following a different trajectory all-together. Apple again has been the undisputed leader in this game with the introduction of first the micro-SIM and now the nano-SIM.

Reproduced from Wikimedia Commons

To be clear here, currently this has not led to any dramatic impact upon the capabilities of the SIM. Advances in technology continue to ensure that more and more information can be squeezed into a smaller and smaller footprint. And although there have been claims that the main purpose was elegance in design and to squeeze more in the limited space that exists I do wonder if there is a long term strategic motive in this move.

Let us revisit the SIM once again; in the broader sense it is a repository of subscriber and network information on a chip. In the modern world of the apps, cloud services and over-the-top updates is there any real USP of having an actual piece of hardware embedded in the phone? This is not a revolutionary thought – in fact Apple was rumored to have thought about it a couple of years ago – and was working towards a SIM-less phone. This concept is not new – some interesting notes about how this could look like can be found back in 2009. From what I gathered was that at that time a strong united ruckus from the carriers dissuaded them from continuing the path.

Two years have passed since then, and you continue to see continued margin pressures from the operators while folks such as Apple and Samsung continue to be the darlings of Wall Street, and well – the SIM card gets smaller and smaller. How does that impact the operator – well for one, if the operators continue to bank on the actual chip as their own property perhaps this advantage would continue to slip away. This is increasingly important since although the SIM could get smaller to accommodate the traditional functions of a SIM – if you then add in other potential functionalities such as payment, security etc then at some point you do need additional real estate to include these functionalities. And at that time if the SIM is just too small, and there are a large number of handset manufacturers (who customers want) who design to this nano spec then well – the operator is out of options.

However, this ‘creative destruction’ as coined by Schumpeter is perhaps the trigger that the telecom operators need in the first place. The E-SIM is perhaps not the end of the game for them, but the advent of a new start. This would be one where software triumphs over hardware – where functionalities are developed and embedded upon multiple operating systems and customized based upon the each individual device and user capabilities. Here rather than mass producing SIMs and having processes to authorize and configure systems users could take any phones and get registered over the air, have capabilities dynamically assigned and configured to suit their specific need. In some ways – it would be the era of mass customization, which can be done efficiently, easily and seamlessly.

It would definitely be a different ball-game, and I can only speculate which way the ball would spin – but perhaps it would be in their own interests for operators to willingly embrace such a transformation rather than push back – the opportunities might simply outnumber the risk.

RIM – a fall from grace

Two news articles piqued my interest last week. First was Marissa Meyer’s (the CEO of Yahoo) announcement that all employees would now be provided by free smart-phones and accompanied data plan. This would be along her priority that Yahoo would have to be a major player in the mobile world by 2015; in order to do so would require that employees use and understand user behavior to create a compelling mobile value proposition. What was telling were the vendors chosen Apple, HTC, Samsung or Nokia….. but no RIM. On top of this Yahoo would now discontinue IT support for the Blackberry platform.

The second was thescripted and belted out by RIM executives for the Blackberry JAM developers’ conference.

I have seen performances, but perhaps never something that sounded so desperate an effort to keep the few developers who haven’t deserted them – as yet. The company has now literally put all its eggs in one basket focusing on the BB10 launch promised for next quarter. If I was a shareholder I would have to ask CEO Thorsten Heins if this is the best punch that he could pack. I am also a bit mystified on their selection of their CEO in the first place – given that he came from Siemens who themselves do not have a stellar track record in this regard and hasn’t done anything radical enough to shake up a company which perhaps desperately needs just that – a different way of looking at their business.

This is just what I will try to postulate; perhaps not rocket science but drawing it up from first principles and positioning it against current competitive trends in this space.

What has been BB’s strength, the USP which drew enterprise customers in hordes during the boom years? It could be summarized as the phone with its ubiquitous keyboard as well as the BBM messaging and email platform offering secure communications prized by enterprise customers. This was the firm belief that this capability would not be replicated and stuck to their strategy over a decade. A decade is light years in the fast moving telecom space. Fast forward a decade later and touch screens are the order of the day with technologies such as swype making typing easier. At the same time 3rd party companies have come up with compelling solutions which offer similar levels of security but are compatible across multiple platforms and/ or are available at a lower price point. Perhaps they do not maintain the BB legendary watertight server structure but for a majority of the populace this is just good enough. At the same time the shift in behavior has ensured that bring-your-own-device (BYOD) is gaining popularity and enterprises are pandering towards the preferences of their employees who prefer an Apple/ Android phone with thousands of apps to the Blackberry. To its own consternation Blackberry has been unsuccessful in wooing developers its platform – ‘no developers – no apps’. On top of this one USP was the ability compress data in order to squeeze data in older 2G – 2.5G network. With the emergence of 3G/ 4G networks media is now the primary bandwidth hog – email is no longer a red flag item. So now RIM is left with a device which few want, with an app platform which looks like a desert compared to the rest and with messenger and secure email no longer being the preferred service. I will admit that I do not have any deep insights into BB10, but perusing the news and blogs leads me to many skeptics and a few optimists. Perhaps it is drawn from past history with many promises and a track record of under-delivery.

So what could RIM do? On talking to present and past BB users one gets the feeling that although people have gotten past the desire for the handsets (now preferring the iPhone and devices from the Samsung/ HTC universe) there is still an appreciation for the neat and effective BBM and email service. Could RIM drop its pretense of being a device company and migrate along with the rest of the world into being the ‘multi-platform app’ for enterprises. Such an app (or an ecosystem of apps) would leverage the ‘security and trustworthiness’ of RIM, would appeal to the broad range of former RIM BB users who loved the service, but perhaps are now users of different handsets.

Of course, this is no Blue Ocean, but RIM does have the background, the brand and the history to deliver such a service. It would mean a harsh restructuring of the company, but RIM would be able to survive – find its mojo and hopefully emerge as a phoenix in the expanding and lucrative billion dollar mobile enterprise universe

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours

Nokia & Microsoft – a failing strategy?

The past few weeks must have been a veritable headache for Stephen Elop and his crew at Nokia, one which would be shared with his former employers at Microsoft. After a lot of ballyhoo, and just one week before the iPhone 5 launch the much vaunted Window 8 phones were finally launched at the Nokia World event. This one was deemed important enough that the Microsoft head honcho, Steve Ballmer attended in person.

The result was a disappointment and the stock market made this amply clear by the end of day. What definitely did not help was Nokia resorting to cheap trickery to ‘enhance’ the feature set or the fact that they would generously dole out around $150 million to carriers to subsidize the device. No small wonder many analysts sent in a buy recommendation, with some trying to figure out the value of Nokia’s patent portfolio determining the lowest price at which they could snatch a bargain. But I do not want to dwell only on the negatives, but instead try to peer through a looking glass to try and gather what could or should they do to change this downward spiral.

Let us look at the bigger and far brighter picture. Although smart-phones adoption is increasing fast at the same time they form a tiny fraction of the total number of phones which stands at around 6 billion! For example in South Africa where I am currently based, only 14% of the total subscriber base own smart-phones. From a market opportunity, well there is certainly a huge untapped market to be explored rather than having to fight for market-share in a saturated environment. Agreed this market is primarily in the developing world – but one market which Nokia has keenly understood for over a decade. Nokia has honed its skills in being able to deliver feature phones at low prices and is a well loved brand in this community. Microsoft too is well known in these circles. Rather than aim for a head-on confrontation with Samsung and Apple in developed markets wouldn’t it be interesting to aim for a Windows 8 touch-screen device in the APAC and Africa regions? Nokia could conceivably energize its much vaunted logistics and R&D to create such a device in a global partnership with Microsoft. This would not be a retreat from a battle, but prepare and establish a strong presence in the smart-devices category in a market which is rapidly growing both in earning power as well as numbers. This would need to extend towards devices more than just smart-phones. The Windows 8 platform could offer just this leverage. You could then conceivable have a similar unified experience (a.k.a. Apple) across all your devices, which could make the whole deal a more compelling value proposition.

Of course, this is not a sure shot win. For starters Nokia needs to be doubly aggressive in this case facing the emerging threat of the Chinese with Android powered devices. I believe the whole hoopla with the developed markets is a sorry distraction in this respect. Microsoft may even need to revisit its Windows sales strategy and business models if it wants to be serious in the mobile business. None of these are easy decisions, some of which sit on top of large egos at the management at both companies. Perhaps it is time for them to learn from their teams in the developing world, realize and seek this opportunity and move swiftly to capture it before it is too late.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours

{kind=link}